Prospect theory

Expansion Funnel Raw 50 → Dedup 22 → NER 19 → Enqueued 17

| Prospect theory | |

|---|---|

| |

| Name | Prospect Theory |

| Field | Behavioral economics, Cognitive psychology |

| Founded | 1979 |

| Founders | Daniel Kahneman, Amos Tversky |

| Key publication | "Prospect Theory: An Analysis of Decision under Risk" in Econometrica |

| Influenced | Behavioral finance, Consumer choice, Public policy |

Prospect theory. It is a behavioral model developed by psychologists Daniel Kahneman and Amos Tversky, published in a seminal 1979 paper in Econometrica. The theory describes how individuals make decisions involving probabilistic outcomes, demonstrating systematic deviations from the predictions of classical Expected utility theory. Its core insights involve how people evaluate potential losses and gains relative to a reference point, leading to risk-averse behavior in domains of gain and risk-seeking behavior in domains of loss.

Introduction to Prospect Theory

The framework emerged as a descriptive challenge to the dominant Neoclassical economics paradigm of rational choice. While traditional models, like those advanced by John von Neumann and Oskar Morgenstern in Theory of Games and Economic Behavior, assumed consistent preferences, the work of Kahneman and Tversky at the Hebrew University of Jerusalem and later Stanford University revealed profound empirical anomalies. Their research, often involving controlled experiments, showed that real human decision-making is heavily influenced by psychological heuristics and biases, such as those documented in their earlier work on Judgment under Uncertainty. This foundational shift provided a more accurate account of choices observed in markets, insurance purchases, and gambling.

Key Concepts and Principles

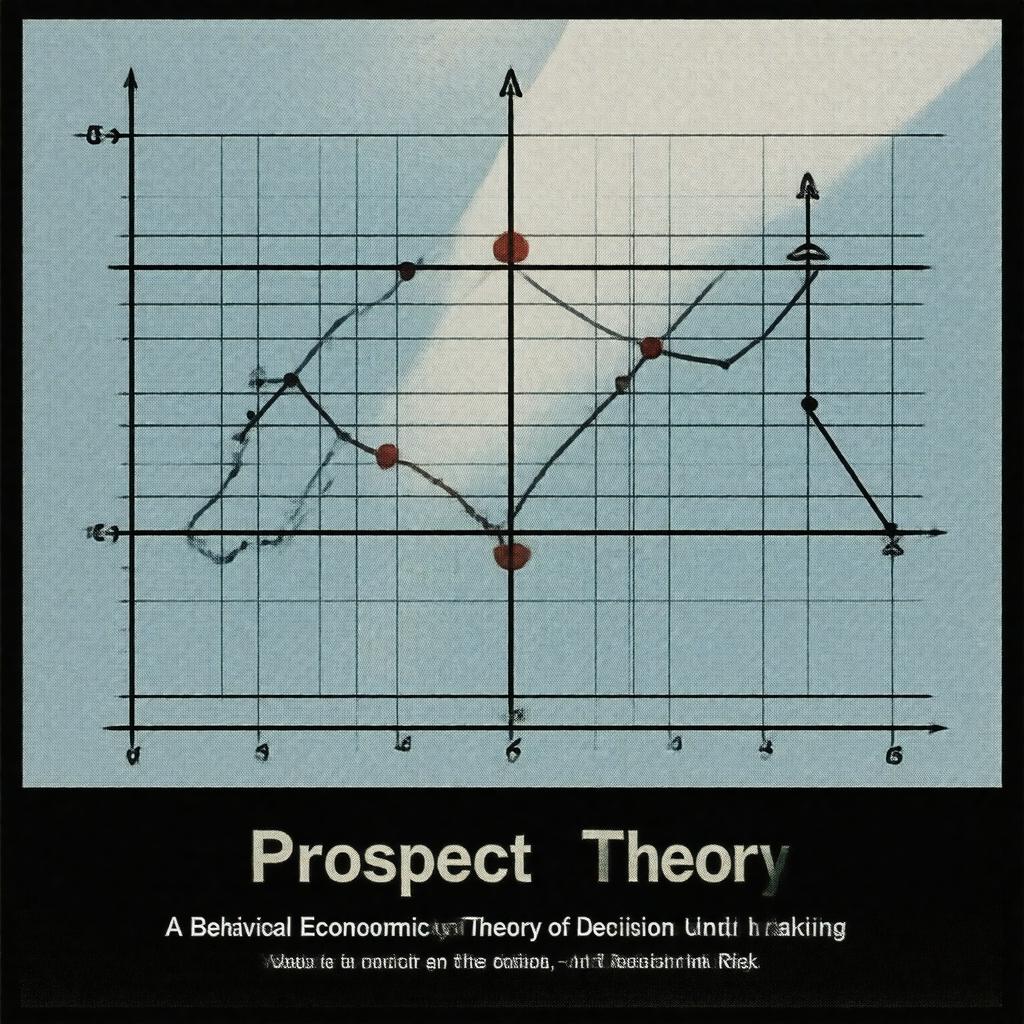

The theory is built upon several interconnected components. The **value function** is defined on deviations from a reference point, is concave for gains and convex for losses, and is steeper for losses, illustrating **loss aversion**. The **probability weighting function** posits that people overweight small probabilities and underweight moderate to high ones, explaining the simultaneous appeal of both lotteries and insurance. Decision-making occurs in two phases: an initial editing phase, where prospects are simplified using operations like Mental accounting, followed by an evaluation phase where the edited prospects are assessed. These principles explain phenomena like the **disposition effect** in Stock market trading and the **endowment effect** documented by Richard Thaler.

History and Development

The intellectual origins lie in the collaboration between Kahneman and Tversky, which began in the late 1960s. Their critique of Expected utility theory culminated in the 1979 Econometrica article, a landmark that bridged Psychology and Economics. This work was significantly expanded in 1992 with the development of **Cumulative prospect theory**, which extended the model to uncertain outcomes with any number of possibilities and incorporated rank-dependent weighting, addressing theoretical issues in the original formulation. The awarding of the Nobel Memorial Prize in Economic Sciences to Kahneman in 2002 and the foundational role of Tversky cemented the theory's status within the Social sciences.

Applications and Implications

The framework has been extensively applied in Behavioral finance to explain market puzzles like the Equity premium puzzle. In Public policy, it informs the design of nudges and default options in programs ranging from Retirement plan enrollment to Organ donation systems, as advocated by the Behavioural Insights Team. It shapes marketing strategies, such as framing discounts as avoiding a loss rather than gaining a saving. The theory also provides insights into international relations, analyzing decisions during crises like the Cuban Missile Crisis, and in legal settings, influencing the design of Tort law and Settlement negotiation strategies.

Criticisms and Challenges

Some economists from the University of Chicago tradition argue that the theory's parameters are difficult to estimate and that learning or market forces may correct individual biases over time. Critics note that the editing phase is less formally specified than the evaluation phase, leading to predictions that can be context-dependent. Alternative models, such as Regret theory developed by Graham Loomes and Robert Sugden, or the more recent Drift diffusion model from Neuroeconomics, offer competing explanations for certain anomalies. Furthermore, cross-cultural studies, including work by researchers at the Max Planck Institute, suggest that the degree of loss aversion may vary across societies.

Comparison to Other Theories

It stands in direct contrast to Expected utility theory, which assumes linear probability weighting and a utility function defined on final wealth. Unlike the normative Von Neumann–Morgenstern utility theorem, it is a descriptive model of actual choices. It shares a focus on psychological realism with Herbert Simon's concept of Bounded rationality but provides a more specific mathematical formulation for decisions under risk. Compared to Mean-variance analysis in Modern portfolio theory, it incorporates the asymmetric impact of losses and gains. While Game theory often assumes perfect rationality, prospect theory has been integrated into behavioral versions to model actors in conflicts or negotiations more accurately.

Category:Behavioral economics Category:Decision theory Category:Psychological theories