Gaussian Distribution

This article was accepted into the corpus but its outbound wikilinks were never NER-processed — typical at the deepest BFS hop or when the run's entity cap was reached. No expansion funnel to show.

| Gaussian Distribution | |

|---|---|

| |

| Name | Gaussian Distribution |

| Type | continuous |

| Parameters | μ (mean), σ² (variance) |

| Support | (-∞, ∞) |

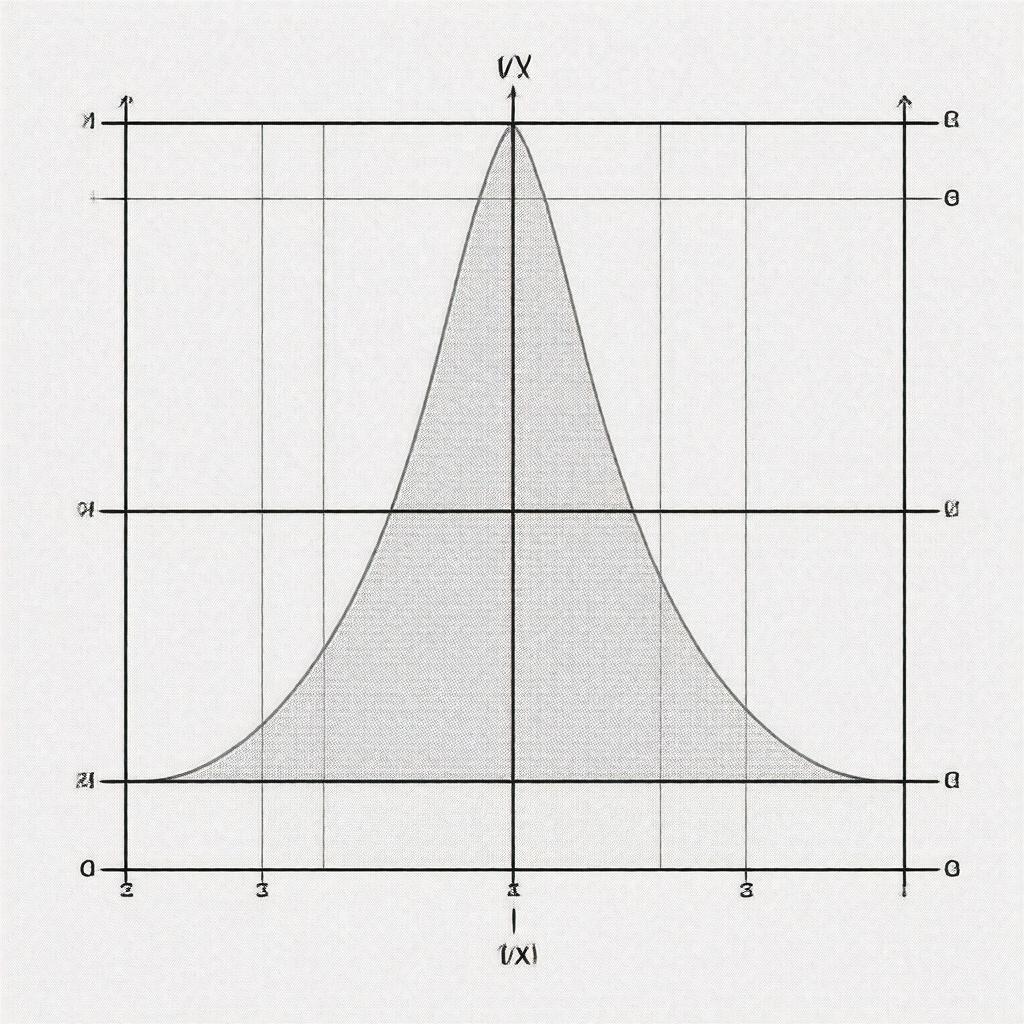

| 1/σ√(2π) * e^(-((x-μ)²)/(2σ²)) | |

| Cdf | Φ((x-μ)/σ) |

| Variance | σ² |

Gaussian Distribution is a fundamental concept in Statistics, Probability Theory, and Data Analysis, extensively used by renowned statisticians like Ronald Fisher, Karl Pearson, and Jerzy Neyman. It is a continuous probability distribution that is commonly observed in many natural phenomena, such as the Normal Distribution of Height in Human Population, and is widely applied in various fields, including Physics, Engineering, and Economics, by prominent figures like Albert Einstein, Stephen Hawking, and Milton Friedman. The Gaussian Distribution is also known as the Normal Distribution or Bell Curve, and its properties have been studied by mathematicians like Carl Friedrich Gauss, Pierre-Simon Laplace, and Andrey Markov. It has numerous applications in Signal Processing, Image Processing, and Machine Learning, as seen in the work of Alan Turing, Marvin Minsky, and Yann LeCun.

Introduction

The Gaussian Distribution is a probability distribution that is symmetric about the mean, showing that data near the mean are more frequent in occurrence than data far from the mean, a concept also explored by Francis Galton and Emile Borel. In Probability Theory, the Gaussian Distribution is a continuous distribution, which means that it can take on any value within a given range, and is often used to model real-valued random variables, as discussed by Andrei Kolmogorov and Henri Lebesgue. The Gaussian Distribution has been applied in various fields, including Biology, Medicine, and Social Sciences, by researchers like Gregor Mendel, Louis Pasteur, and Émile Durkheim. It is also used in Finance and Economics to model stock prices and returns, as seen in the work of Eugene Fama, Myron Scholes, and Robert Merton.

Definition

The Gaussian Distribution is defined by its probability density function (pdf), which is given by the formula: f(x) = 1/σ√(2π) * e^(-((x-μ)²)/(2σ²)), where μ is the mean, σ is the standard deviation, and x is the variable, a concept also studied by David Hilbert and Hermann Minkowski. The Gaussian Distribution can be characterized by its mean and variance, which are used to describe the shape and spread of the distribution, as discussed by Abraham Wald and Jacob Wolfowitz. The Gaussian Distribution is often denoted as N(μ, σ²), where N represents the normal distribution, and μ and σ² are the parameters of the distribution, a notation used by John von Neumann and Norbert Wiener. It is also related to other distributions, such as the Chi-Squared Distribution, Student's T-Distribution, and F-Distribution, which are used in Hypothesis Testing and Confidence Intervals, as seen in the work of R.A. Fisher and Henry Scheffé.

Properties

The Gaussian Distribution has several important properties, including symmetry, unimodality, and infinite support, which make it a useful model for many real-world phenomena, as discussed by George Box and George Jenkins. The Gaussian Distribution is also stable under addition, meaning that the sum of two independent Gaussian random variables is also Gaussian, a property used by Claude Shannon and Edwin Jaynes. Additionally, the Gaussian Distribution has a number of interesting properties, such as the fact that the mean, median, and mode are all equal, and that the distribution is invariant under affine transformations, as studied by David Blackwell and Lloyd Shapley. The Gaussian Distribution is also closely related to other distributions, such as the Lognormal Distribution and Exponential Distribution, which are used to model Skewed Data and Survival Analysis, as seen in the work of Frank Wilcoxon and John Tukey.

Applications

The Gaussian Distribution has numerous applications in various fields, including Signal Processing, Image Processing, and Machine Learning, as seen in the work of Yann LeCun, Geoffrey Hinton, and Andrew Ng. It is used to model real-valued random variables, and is often used in Hypothesis Testing and Confidence Intervals, as discussed by Jerzy Neyman and Egon Pearson. The Gaussian Distribution is also used in Finance and Economics to model stock prices and returns, and to estimate Volatility and Risk, as seen in the work of Robert Engle and Clive Granger. Additionally, the Gaussian Distribution is used in Biology and Medicine】 to model the distribution of Gene Expression and Disease Prevalence, as studied by Francis Crick and James Watson.

Related_Distributions

The Gaussian Distribution is related to several other distributions, including the Chi-Squared Distribution, Student's T-Distribution, and F-Distribution, which are used in Hypothesis Testing and Confidence Intervals, as seen in the work of R.A. Fisher and Henry Scheffé. It is also related to the Lognormal Distribution and Exponential Distribution, which are used to model Skewed Data and Survival Analysis, as discussed by Frank Wilcoxon and John Tukey. Additionally, the Gaussian Distribution is related to the Poisson Distribution and Binomial Distribution, which are used to model Count Data and Binary Data, as studied by Siméon Poisson and Jacob Bernoulli. The Gaussian Distribution is also closely related to other distributions, such as the Cauchy Distribution and Laplace Distribution, which are used to model Heavy-Tailed Data and Robust Statistics, as seen in the work of Augustin-Louis Cauchy and Pierre-Simon Laplace.

History

The Gaussian Distribution has a long and rich history, dating back to the work of Carl Friedrich Gauss and Pierre-Simon Laplace in the 18th century, who used it to model Astronomical Data and Error Theory, as discussed by Adrien-Marie Legendre and Joseph-Louis Lagrange. The Gaussian Distribution was later developed and applied by statisticians like Ronald Fisher, Karl Pearson, and Jerzy Neyman, who used it to develop Statistical Inference and Hypothesis Testing, as seen in the work of Egon Pearson and George Snedecor. The Gaussian Distribution has also been applied in various fields, including Physics, Engineering, and Economics, by prominent figures like Albert Einstein, Stephen Hawking, and Milton Friedman, and has been used to model a wide range of phenomena, from the Normal Distribution of Height in Human Population to the Stock Market and Economic Growth, as studied by Eugene Fama and Robert Shiller. Category:Probability distributions