prospect theory

This article was accepted into the corpus but its outbound wikilinks were never NER-processed — typical at the deepest BFS hop or when the run's entity cap was reached. No expansion funnel to show.

| prospect theory | |

|---|---|

| |

| Name | Prospect theory |

| Authors | Daniel Kahneman; Amos Tversky |

| Year | 1979 |

| Field | Behavioral economics; Decision theory; Psychology |

| Notable work | "Prospect Theory: An Analysis of Decision under Risk" |

prospect theory Prospect theory is a descriptive model of decision making under risk developed to explain observed deviations from expected utility maximization in human choices. It originated in a collaboration between Daniel Kahneman and Amos Tversky and has influenced research across Nobel Memorial Prize in Economic Sciences, American Psychological Association, University of California, Berkeley, Hebrew University of Jerusalem, Stanford University, and Princeton University. The theory contrasts with classical models associated with John von Neumann and Oskar Morgenstern and informed later work by scholars linked to Behavioral finance and Cognitive psychology.

Overview

Prospect theory proposes that people evaluate potential outcomes relative to a reference point rather than by final wealth, integrating empirical patterns demonstrated in experiments by Kahneman and Tversky associated with the Cognitive revolution debates and research programs at institutions such as University of Michigan, University College London, Massachusetts Institute of Technology, Columbia University, and Harvard University. It introduces psychologically grounded constructs—reference dependence, loss aversion, diminishing sensitivity, and probability weighting—that challenge assumptions in frameworks developed by Leonid Kantorovich and later formalized in work following Expected utility hypothesis traditions. The theory’s initial publication appeared in a journal connected to major scholarly outlets like American Economic Association symposia and spurred applications across domains involving actors from U.S. Securities and Exchange Commission, World Bank, International Monetary Fund, European Central Bank, and Bank of England.

Core Concepts and Mathematical Formulation

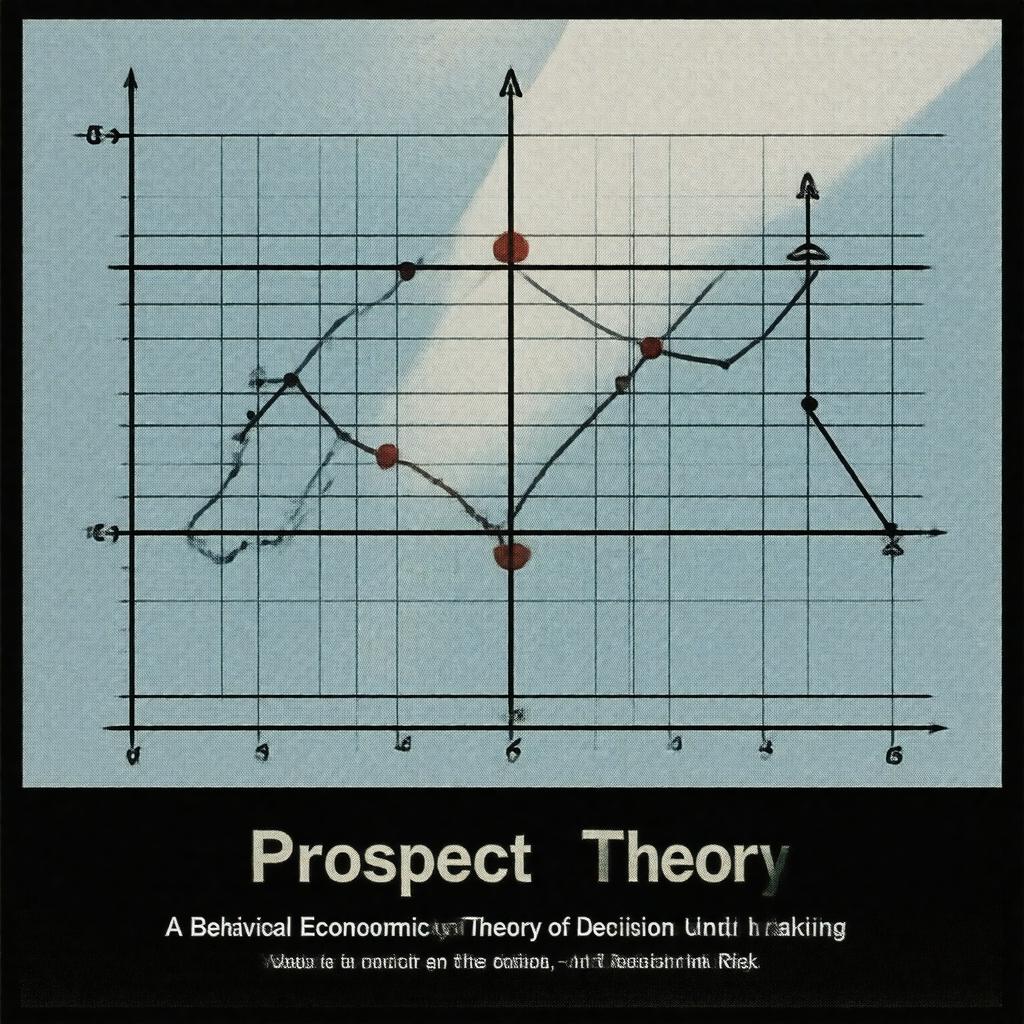

Prospect theory models choices via a value function defined on gains and losses relative to a reference point and a probability weighting function that transforms objective probabilities; these ideas contrast with utility functions used by John Hicks and probability axioms explored by Andrey Kolmogorov and Bruno de Finetti. The value function is typically concave for gains and convex for losses, steeper for losses than gains, reflecting loss aversion similar to observations in experiments stemming from collaborations at Hebrew University of Jerusalem and subsequently examined at University of Chicago, Yale University, and University of Pennsylvania. The probability weighting function captures overweighting of small probabilities and underweighting of moderate to high probabilities; this empirical regularity links to experimental paradigms used by teams at Max Planck Society, Carnegie Mellon University, Northwestern University, and University of California, Los Angeles. Formal representations include parameters estimated by methods related to econometric techniques popularized at London School of Economics, Cowles Commission, and statistical approaches tied to Ronald Fisher and Jerzy Neyman. Cumulative prospect theory refines the original model by using cumulative probabilities and rank-dependent transformations, building on ideas from scholars associated with Allais paradox discussions and work by researchers with ties to Université Paris-Sorbonne and University of Amsterdam.

Empirical Evidence and Experimental Findings

Laboratory and field experiments supporting prospect-theoretic predictions have been conducted in settings connected to RAND Corporation, Bell Labs, SRI International, National Bureau of Economic Research, and experimental labs at MIT Sloan School of Management, Columbia Business School, and London School of Economics. Classic findings include choices in framed gambles demonstrating loss aversion and reference dependence, replications in studies from University of Oxford, University of Cambridge, Australian National University, and cross-cultural work sponsored by institutions like World Health Organization and United Nations programs. Empirical challenges emerged through large-scale datasets analyzed in collaborations involving Google, Microsoft Research, Facebook, and financial markets data from New York Stock Exchange, NASDAQ, and London Stock Exchange where probability weighting and reference effects are tested against market behavior documented by researchers affiliated with Princeton University and University of Chicago Booth School of Business.

Applications and Implications

Prospect theory has informed policy and institutional design at entities such as U.S. Department of the Treasury, European Commission, Organisation for Economic Co-operation and Development, and Federal Reserve System by shaping insights used in behavioral interventions advocated by proponents linked to Behavioral Insights Team and White House Office of Science and Technology Policy. In finance, the theory influenced models of investor behavior studied in contexts involving Goldman Sachs, JP Morgan Chase, BlackRock, and academic centers like Wharton School and INSEAD. It also guided research in negotiation and legal decision making at Harvard Law School, Yale Law School, and arbitration institutions including International Court of Arbitration. Health economics, marketing, and environmental policy applications draw on prospect-theoretic framing in projects supported by National Institutes of Health, Bill & Melinda Gates Foundation, and United Nations Environment Programme.

Criticisms and Extensions

Critics associated with traditions at Chicago School of Economics, Virginia School, and skeptics influenced by work at London School of Economics have questioned the theory’s normative implications, parameter stability, and predictive power in large-scale markets such as those overseen by Securities and Exchange Commission and central banks like Bank of Japan. Extensions include cumulative prospect theory, models blending prospect theory with Expected utility theory traditions, and alternative accounts leveraging concepts from researchers at MIT, Stanford Graduate School of Business, and Columbia University that incorporate learning dynamics, reference-point formation, and neural mechanisms explored at National Institutes of Health and Max Planck Institute for Human Cognitive and Brain Sciences. Ongoing debates involve experimental reproducibility pursued by teams at Center for Open Science, meta-analyses coordinated by Cochrane Collaboration, and theoretical generalizations linked to scholars awarded prizes like the Nobel Memorial Prize in Economic Sciences.