1929 stock market crash

Generated by GPT-5-mini

Generated by GPT-5-miniExpansion Funnel Raw 96 → Dedup 0 → NER 0 → Enqueued 0

| 1929 stock market crash | |

|---|---|

| |

| Name | Crash of 1929 |

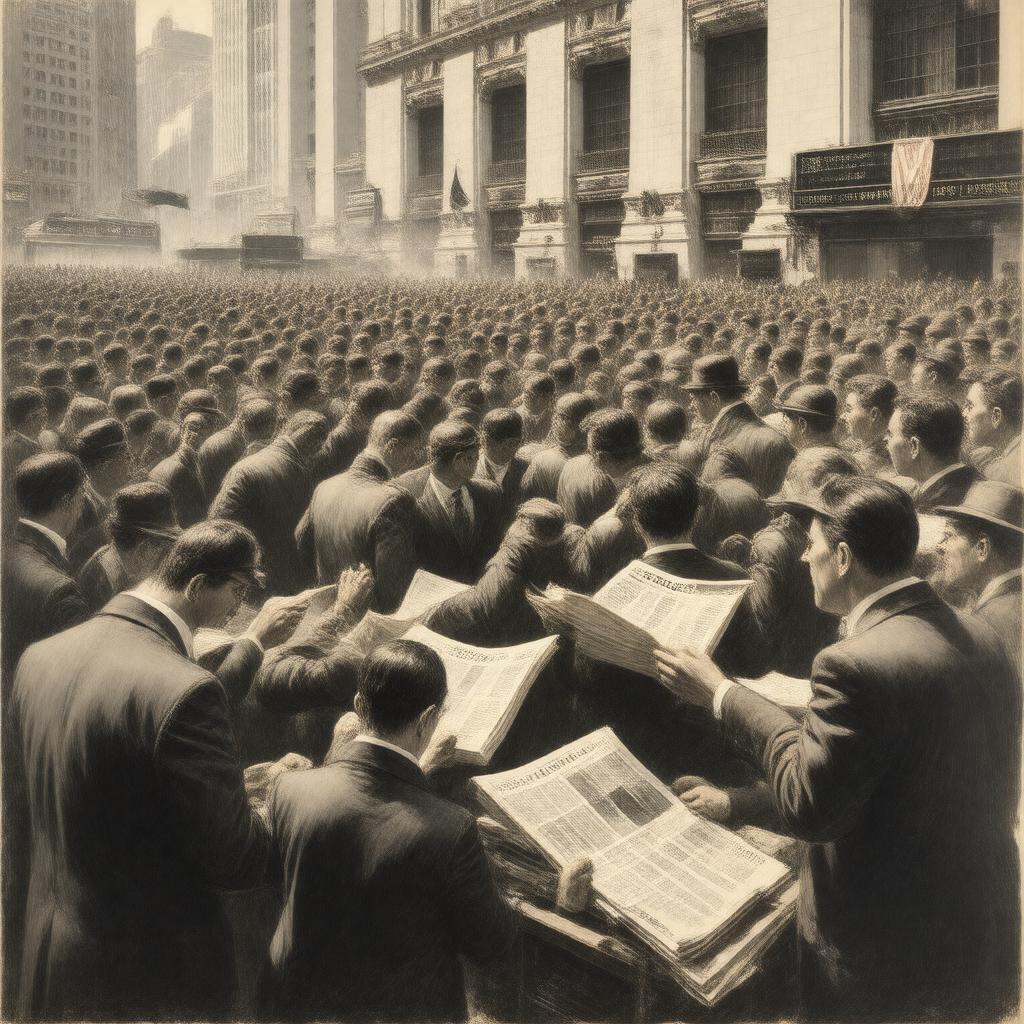

| Caption | Traders on the floor of the New York Stock Exchange in October 1929 |

| Date | October–November 1929 |

| Location | New York City, New York (state), United States |

| Type | Financial crash |

| Outcome | Widespread market losses; bank failures; policy reforms |

1929 stock market crash The 1929 collapse on the New York Stock Exchange precipitated a severe financial contraction that coincided with the onset of the Great Depression. Major actors during the episode included prominent investors such as Jesse Livermore, financiers associated with J.P. Morgan & Co., and public officials in Washington, D.C. including appointees linked to the Herbert Hoover administration. The crash catalyzed policy debates among figures in institutions like the Federal Reserve System and led to regulatory innovations embodied in legislation associated with the Franklin D. Roosevelt era.

Background and causes

Speculative excesses in the 1920s involved market participants such as brokers at the New York Stock Exchange and firms like Lehman Brothers and Goldman Sachs engaging in margin buying, while corporate leaders at General Electric, U.S. Steel, and American Telephone and Telegraph Company promoted equity issuance. Monetary conditions set by the Federal Reserve Board interacted with credit flows from banks including Bank of United States and institutions linked to J.P. Morgan & Co., amplifying leverage. Structural strains in industries such as railroads, exemplified by Pennsylvania Railroad, and commodities markets tied to producers like Anaconda Copper revealed uneven profitability. Regulatory frameworks overseen by bodies associated with New York City banking elites lacked mechanisms found later in statutes like the Securities Act of 1933 and the Securities Exchange Act of 1934. Intellectual currents from economists at University of Chicago and commentators in outlets such as the New York Times and The Wall Street Journal shaped investor sentiment, as did public figures including Andrew Mellon and Charles E. Mitchell.

Timeline of the crash (October–November 1929)

In early October 1929 trading volatility at the New York Stock Exchange intensified after heavy declines in stocks of companies such as Union Pacific Railroad, Republic Steel, and General Motors. On days of panic traders, including speculative operators influenced by reports from Associated Press and wire services, overwhelmed clearing mechanisms at banks such as Guaranty Trust Company of New York. Interventions by financiers aligned with J.P. Morgan & Co. and meetings at the offices of figures like Charles E. Mitchell briefly supported prices. The largest single-session drops followed intense selling pressure from margin calls executed by brokerage houses including firms similar to E.F. Hutton and Merrill Lynch. By November, market capitalization losses had affected insurance companies like MetLife and savings institutions such as Equitable Trust Company, while credit contraction spread through corridors of Wall Street into commercial lending networks centered in Manhattan.

Economic and financial consequences

Stock market losses fed into bank runs that impacted institutions including the Bank of United States and regional banks in Midwestern United States cities like Cleveland and Chicago. Collapses among brokerage houses and failures of companies such as Nash Motors and smaller manufacturers curtailed investment and industrial output, affecting payrolls at firms like Ford Motor Company and leading to rising unemployment measured in urban centers such as New York City and Detroit. International finance links through entities like the Bank of England and institutions involved in reparations from the Treaty of Versailles transmitted strains to European markets, diminishing trade flows monitored by the League of Nations secretariat and manifesting in deflationary pressures documented by economists at London School of Economics and Harvard University. Corporate bankruptcies and declines in commodity prices hurt agricultural interests represented by groups like the American Farm Bureau Federation.

Government and regulatory responses

Initial policy responses involved deliberations among officials at the Federal Reserve System and advisers to President Herbert Hoover, with voices from Secretary of the Treasury Andrew Mellon and Treasury staff influencing decisions on liquidity support. Later legislative and institutional reforms under President Franklin D. Roosevelt included creation of agencies and statutes associated with the Securities Act of 1933, the Securities Exchange Act of 1934, and the establishment of the Securities and Exchange Commission. Banking reforms drew on models linked to the Glass–Steagall Act and the chartering of the Federal Deposit Insurance Corporation, shaped by congressional leaders such as Senator Carter Glass and Representative Henry Steagall. Debates in United States Congress and among academics at Columbia University and Princeton University influenced regulatory architecture governing capital markets and deposit insurance.

Social and cultural impact

The crash and ensuing depression altered public life in urban areas like New York City, Chicago, and San Francisco, affecting cultural institutions such as Radio Corporation of America and entertainment venues tied to Hollywood, including studios like Metro-Goldwyn-Mayer. Labor movements represented by the American Federation of Labor and community organizations in neighborhoods of Brooklyn and Bronx confronted high unemployment and foreclosures affecting families tied to unions at plants such as Bethlehem Steel. Literary and artistic responses emerged from authors and artists associated with institutions like the New School and publications including The New Yorker and Harper's Magazine, while documentaries in later decades examined experiences captured by photographers at the Farm Security Administration.

International effects and global transmission

Financial contagion spread from New York City to financial centers including London, Paris, Berlin, and Tokyo through credit lines managed by correspondent banks tied to J.P. Morgan & Co. and European clearinghouses. Gold flow dynamics involving the Bank of England and policies in nations such as France and Germany constrained monetary responses, while trade contractions affected export-dependent economies like Argentina, Brazil, and Chile. Political repercussions influenced policymakers in capitals including Ottawa, Canberra, and Rome, and contributed to instability in countries experiencing banking crises such as Austria and Hungary.

Legacy and historical interpretations

Scholars at institutions including University of Cambridge, Princeton University, and Yale University have debated whether the crash was a primary cause of the Great Depression or a catalyst interacting with factors highlighted by economists like John Maynard Keynes, Milton Friedman, and Irving Fisher. Interpretations range from emphasis on credit contraction documented by research from National Bureau of Economic Research to institutional failings underscored in work associated with Securites Regulation histories and biographies of financiers like Jesse Livermore and Charles E. Mitchell. The episode shaped subsequent policy orthodoxy in central banking at the Federal Reserve System and regulatory practice at the Securities and Exchange Commission, leaving a lasting imprint on financial history curricula at universities such as Columbia University and Harvard University.

Category:1929 Category:Financial crises