Prospect theory

This article was accepted into the corpus but its outbound wikilinks were never NER-processed — typical at the deepest BFS hop or when the run's entity cap was reached. No expansion funnel to show.

| Prospect theory | |

|---|---|

| |

| Name | Prospect theory |

| Field | Behavioral economics, Cognitive psychology |

| Developed by | Daniel Kahneman, Amos Tversky |

| Year | 1979 |

| Journal | Econometrica |

| Related theories | Expected utility theory, Cumulative prospect theory, Regret theory |

Prospect theory is a behavioral model of decision-making under risk, developed as a descriptive alternative to Expected utility theory. Formulated by psychologists Daniel Kahneman and Amos Tversky and published in 1979 in the journal Econometrica, it systematically explains a range of observed choices that violate standard economic rationality. The theory posits that people evaluate potential losses and gains using heuristics, leading to decisions that are reference-dependent and influenced by nonlinear probability weighting.

Overview and key concepts

The framework was introduced through a series of experiments by Daniel Kahneman and Amos Tversky at Hebrew University and later Stanford University, challenging the axioms of Expected utility theory proposed by scholars like John von Neumann and Oskar Morgenstern. Central to the model are the concepts of editing and evaluation phases, where prospects are first simplified and then assessed. Decisions are made relative to a subjective reference point, often the status quo, rather than final wealth. This work contributed significantly to the rise of Behavioral economics and influenced subsequent research at institutions like the University of Chicago and Massachusetts Institute of Technology. Kahneman's contributions were recognized with the Nobel Memorial Prize in Economic Sciences in 2002.

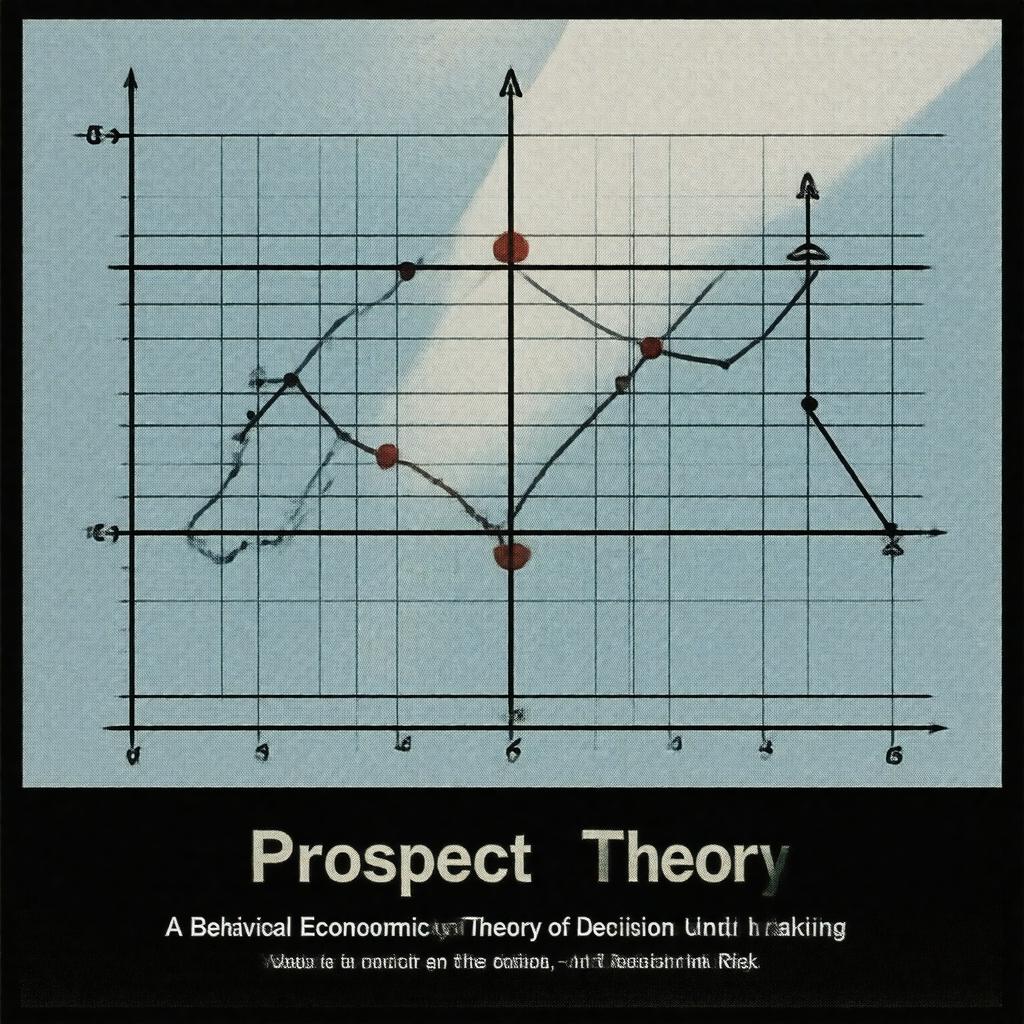

Value function and loss aversion

The value function is defined on deviations from a reference point and is typically S-shaped. It is concave for gains, indicating diminishing sensitivity, and convex for losses, but steeper for losses than for gains—a property termed loss aversion. This asymmetry, quantified by Daniel Kahneman and Amos Tversky, means the pain of losing a sum is psychologically more impactful than the pleasure of gaining the same sum. This principle helps explain phenomena like the Endowment effect, where people value owned items more highly, and the Disposition effect in Stock market trading observed by Hersh Shefrin and Meir Statman. The concept also underpins behaviors in Insurance markets and reactions to Tax policy.

Probability weighting function

Individuals do not treat objective probabilities linearly; instead, they use a weighting function that overweights small probabilities and underweights moderate to high ones. This nonlinear transformation, distinct from the objective probabilities used in Expected utility theory, explains simultaneous gambling and insurance purchasing. People may overvalue tiny chances of large gains, as in Lottery play, while also overvaluing tiny chances of large losses, driving demand for Insurance against low-probability events. This weighting contributes to anomalies like the Allais paradox, first described by Maurice Allais, and is formalized differently in later models like Cumulative prospect theory developed by Daniel Kahneman and Amos Tversky.

Applications and evidence

The theory has been extensively applied across diverse fields. In Finance, it models the Equity premium puzzle and patterns in the S&P 500. In Consumer behavior, it explains pricing strategies and marketing effects. Within Public policy, it informs the design of Nudge theory and frameworks like the United Kingdom's Behavioural Insights Team. Evidence from neuroeconomics, using tools like Functional magnetic resonance imaging, has identified neural correlates in brain regions such as the Amygdala and Prefrontal cortex. Field studies in settings like the Israeli Defense Forces and experiments by Richard Thaler on mental accounting provide further empirical support, influencing practices in Organizational behavior and Negotiation.

Criticisms and extensions

Critics argue the original model can be intransitive and lacks a comprehensive theory for riskless choice. Scholars like David M. Grether and Charles R. Plott have questioned its predictive power in certain market contexts. Major extensions include Cumulative prospect theory, which incorporates rank-dependent weighting and extends the model to continuous distributions. Other models, such as Regret theory advanced by Graham Loomes and Robert Sugden, and Third-generation prospect theory by Abdellaoui Mohammed, offer alternative accounts. The theory's parameters have been estimated in diverse populations, from traders on the New York Stock Exchange to subjects in Tokyo, refining its descriptive accuracy and scope.

Category:Behavioral economics Category:Decision theory Category:Economics theories